Solo_Super

thesis

My Purchase Rating for Arista Networks (NYSE: ANET) has worked fine so far. In February, I had a price target of $171, which was subsequently achieved in less than a month. As my price target is now hit, and the business has been very good – just as I expected – I continue to recommend a buy rating, albeit with a downsizing as the upside potential is now lower than in February.

Results/Help/My Perspectives

With revenues above expectations in Q1 23 and guidance for Q2 23, ANET showed strong operating performance, which I believe is primarily due to the improvement in the supply environment. I believe ANET will be able to more effectively manage its expanded backlog and realize better margins (over time) as a result of these favorable conditions. Also, despite concerns about the challenging macro environment, they are very concerned encouraged by comments from management that there is no problem with demand in 2H23. This is a strength as it de-risks the FY23 guidance, meaning that the consensus that had a more bearish view on the weak impact of the macro backdrop in 2H23 will now revise their estimates. However, despite the positives in relation to execution and the limited question headwinds, I have 2 concerns. The first is the high inventory position. The opportunity to return to a normalized gross margin is likely to be limited by continued inventory build-up as a result of long-term supply contracts (instituted during the supply crunch). The second is demand normalization for Cloud Titan. That said, this shouldn’t be a major concern in the long run. Looking ahead over the long term, I continue to expect the growing importance of AI workloads among cloud users, faster production upgrades of data center switching products, and increased market share with enterprise customers will translate in robust growth.

Gross margin

Returning to my previous point about rising inventories putting pressure on gross margin, a key factor in this trend has been the company’s massive purchasing commitments set in the past two years. In the past, when stocks were low, ANET placed many orders at artificially inflated prices. Eventually, this increased COGS will be transferred from the balance sheet to the profit and loss account, as is obvious to anyone with even a rudimentary understanding of accounting. As a result, gross margin is expected to decrease. These high levels of inventory not only strain ANET’s gross margins, but also prevent the company from deploying valuable working capital elsewhere. As a result, this is a major cause for concern regarding the potential for near-term margin pressure (I understand that management expects sequential improvement in gross margin, but I’m not 100% convinced just yet).

Cloud Titan

Not only was the gross margin pressure something to worry about, but another small concern I have is that Cloud Titan’s revenue growth isn’t quite as strong anymore. I mean this is not exactly surprising as the delivery time was due to the supply chain constraint. However, it’s worth noting that ANET’s Cloud Titan customers have less than six months of exposure at this point. What was once a bullish factor for ANET (because it has great order visibility and investors can better model financials), has now turned into a potential bearish factor. First, with less visibility, investors tend to be more conservative in their estimates. Secondly, the fact that lead times are getting shorter means that the underlying supply chain is actually improving. In a normalized supply environment, customers are less likely to hold more inventory. This could be a short-term demand headwind for ANET in 2H23/1H24 as it faces stiff competition due to the impact on the supply chain.

AI Contribution to growth

Despite some short-term challenges, I believe ANET is well positioned to capitalize on the growing relevance of AI in the networking industry. I expect networking to receive a larger percentage of Cloud Titan’s budget as its importance to supplying data to GPUs grows. ANET’s leading position in high-speed networks is a major differentiator that can help the company capture a sizable portion of this market, in my view. ANET’s AI switching portfolio, especially the 7800 series, began to see significant deployments in production environments in 2023 after undergoing extensive testing and simulations in 2022. As the application of AI develops, I expect this trend to accelerate. In fact, management’s expectation of a sizable contribution from AI this year is the best indicator of AI’s impact on ANET.

Assessment

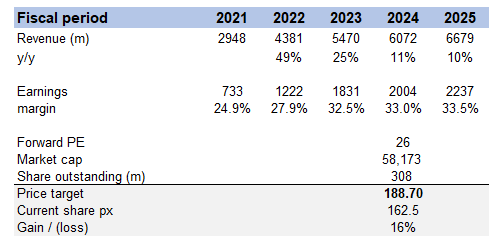

My new model is mainly being updated for faster growth over the next few years as a result of the AI contribution improving in AF25, which I’m quite optimistic about. However, I expect margins to suffer as high-priced inventory hits P&L in FY23, but margins should gradually improve as things stabilize. Another assumption that has been updated is the PE forward at which it should trade. Previously I calculated 24x forward XP. Given management’s balanced demand outlook, I believe 26x should be supported at least through the end of the year.

Own model

Conclusion

Bottom line, my buy assessment for ANET has so far paid off, with the stock hitting my $171 price target within a month. Despite the lower upside potential compared to February, I still recommend a buy rating, albeit with a smaller position size. ANET demonstrated solid operating performance, exceeding revenue expectations in 1Q23 and providing positive guidance for 2Q23. While there are concerns about elevated inventory levels and potential near-term margin pressure, ANET’s long-term growth prospects remain robust. The growing importance of AI workloads, accelerated deployment of AI switching products, and growing market share with enterprise customers position ANET for future success.

#Arista #Networks #Margin #Concerns #Short #Term #Long #Term #Positive #NYSEANET